The French Economy by 2025: Macroeconomic projections 2022-2025.

At the end of December 2022, the Banque de France published its “Macroeconomic projections 2022-2025” (available only in french Projections macroéconomiques 2022-2025 ). It is a report expected by the actors of the French economy, in particular companies for the needs of their strategic plans and/or industrial and commercial plans (PIC or S&OP). In the same vein as several other economic centres, this report shows that the French economy will experience a marked slowdown in 2023. But the Banque de France foresees a recovery in 2024 and 2025.

Note that, in a previous post in June 2022, we reviewed the methodology of the medium-term macroeconomic forecasts for France produced by the Banque de France.

Economic activity in France and Europe will experience a marked slowdown in 2023, then pick up again in 2024 and 2025.

Here are the highlights of this Banque de France report.

▪ “The French economy is undergoing a significant external levy shock of at least 1.5% of GDP, mainly due to the sharp rise in energy prices in Europe, a consequence of the Russian war in Ukraine. This results in excessively high inflation and a drain on the real incomes of companies and households, to a large extent, however, cushioned by public finances.

▪ After a good resilience during most of 2022, activity should go through two distinct phases: a sharp slowdown from this winter, then a decline in inflationary pressures and a gradual resumption of economic expansion in 2024 and especially in 2025.

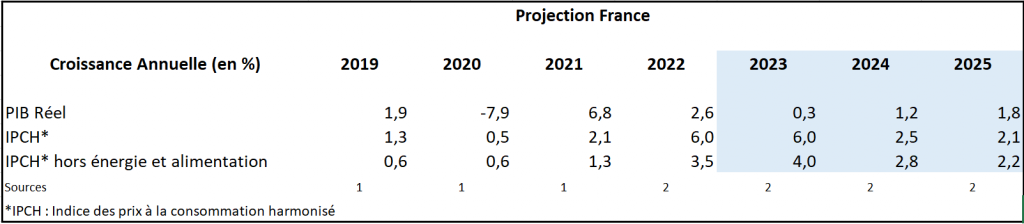

▪ Tensions on international commodity prices, even if they have partially eased since September, have resulted in continuously rising inflation over the year 2022, which should stand at an annual average of 6.0%. This would remain at the same annual average level in 2023, but its year-on-year profile would be very different, with a peak in the first half of 2023 then a sharp decline thereafter (around 4% at the end of the year). In 2024, inflation should continue to fall, even if certain food prices, but also the prices of services, should remain dynamic. At the end of 2024 and in 2025, inflation would return to the European Central Bank (ECB) target of 2%.

▪ Average annual GDP growth should stand at 2.6% in 2022, driven by the resilience of demand and the rebound in the services sector, even if the slowdown in activity was quite marked in the second half of the year. In this context, net job creations have remained strong and the unemployment rate has returned to a historically low level for France (7.3% in 2022).

▪ With the full effect of the external shock, the year 2023 would record a marked slowdown, and GDP growth would only reach +0.3%. Such a projection is surrounded by a still large uncertainty, in particular linked to the vagaries of gas supply quantities and prices: we therefore retain a range of between -0.3% and +0.8% for this forecast of growth in 2023. We cannot therefore exclude the possibility of a recession, which would however then be temporary and limited.

▪ Once the peak of tensions on commodity prices and energy supply has passed, the recovery phase would begin in 2024. It would initially be at a moderate pace, of 1.2% on average per year . The growth dynamic should continue throughout 2025, with average annual GDP growth of 1.8%.

▪ Despite the successive shocks recorded since 2020, the French economy should show resilience over the medium period in terms of employment, household purchasing power and, by 2025, the margin rate of companies. However, this would cover disparities between categories of households and between sectors of activity for companies.

This resilience would have a counterpart relating to the protective role played by public finances: the public debt ratio, already greatly deteriorated following the Covid shock, would thus be stabilized at best by 2025.

Despite the end of the generalized support measures of the tariff shield type, the public expenditure ratio, at 56% of GDP in 2025, could still be two points higher than its pre-Covid level (for a little more than half due to the increase in public expenditure excluding interest charges). »

(1) INSEE et (2) Banque de France

Les principaux points sur les perspectives en France selon la Banque de France

- The external shock linked to the terms of trade induces an ex ante levy of around at least 1.5% of GDP on the French economy in 2022.

- Inflation should peak in H1 2023, before falling back to around 2% at the end of 2024 and in 2025.

- Nominal wages should rise sharply over the entire forecast horizon.

- After a limited decline in 2022-2023, the average purchasing power of households should rise again in 2024-2025.

- After the generally favorable 2019-2021 years, the rises in production costs combined with the virtual absence of productivity gains should weigh on corporate margins in 2022-2023, before a certain normalization.

- A temporary rise in unemployment linked to changes in activity and productivity.

- The public deficit should remain deteriorated in 2022-2023, despite the end of the Covid-19 support measures, under the effect of the continuation of the stimulus measures and those taken to protect the economy against inflation. Based on the information we have at this stage, the public debt ratio would remain around 112% of GDP over the forecast horizon.

- High and persistent uncertainty, particularly on energy prices and supplies”.

- All the details of this report in “Macroeconomic projections 2022-2025”.

The study is posted in French « Projections macroéconomiques 2022-2025 ».